The banking industry is in the middle of a digital evolution, where only the most efficient and adaptive will survive. Conversational banking is a solution to this cultural and behavioural shift, and not just another tech trend to adopt. Approaching it as such is a narrow and misguided understanding of the state of the industry.

Banks insist on investing in tools like IVR (if you don’t know, it’s the voice system that attempts to serve you when phoning into a company)— even when the data shows that their customers hate it. If they zoom out, they realize that their tools are ill-matched for today’s banking customers, and that there are more effective alternatives available.

The paradigm shift in banking

Fintechs have a real shot at disrupting retail banking. And, it's not because they offer similar services at lower costs through digital-only experiences. It's because they're changing what banking means to people.

The biggest threat to incumbent banks is their tendency to lose sight of the bigger picture. Focusing on only products and services and not the entire business model will be their undoing.

Looking for innovation in all the wrong places

The gap that exists between banks and customers is clear, and it's most obvious when we look at the tools they're investing in.

For example, despite the fact that IVR (Interactive Voice Response) is so unpopular, banks continue to invest in it.

Vonage research recently revealed just how bad IVR is for business. The study found that 63% of people believe that reaching an IVR menu makes for a poor experience. What's more, this leads more than half to abandon the company altogether.

Of the customers who ditched a business as a result of reaching an IVR menu, 89% of them spent their money with a competitor.

That's a huge deal, especially for banks. The average acquisition cost of a retail banking customer is roughly $200.

Why -- when other, more preferred and more pervasive channels exist -- do banks force customers to use IVR?

Banks investing in IVR is symptomatic of a larger issue. They're not prioritizing the holistic customer experience. Again, they're focusing on improving legacy systems without regard for the larger picture.

A holistic approach is necessary for banks to be disruptive

Traditional banks must reimagine and reshape their customer experiences. And, they need to start with what their customers actually want. Spoiler alert: they don't want more IVR.

Customers want and expect seamless services. They expect quick answers to simple questions. They don't want to have to go to physical branches. In short, they want streamlined transactions at all touchpoints.

Where conversational banking fits in

After banks do some big-picture thinking, conversational banking emerges as a key piece of the puzzle.

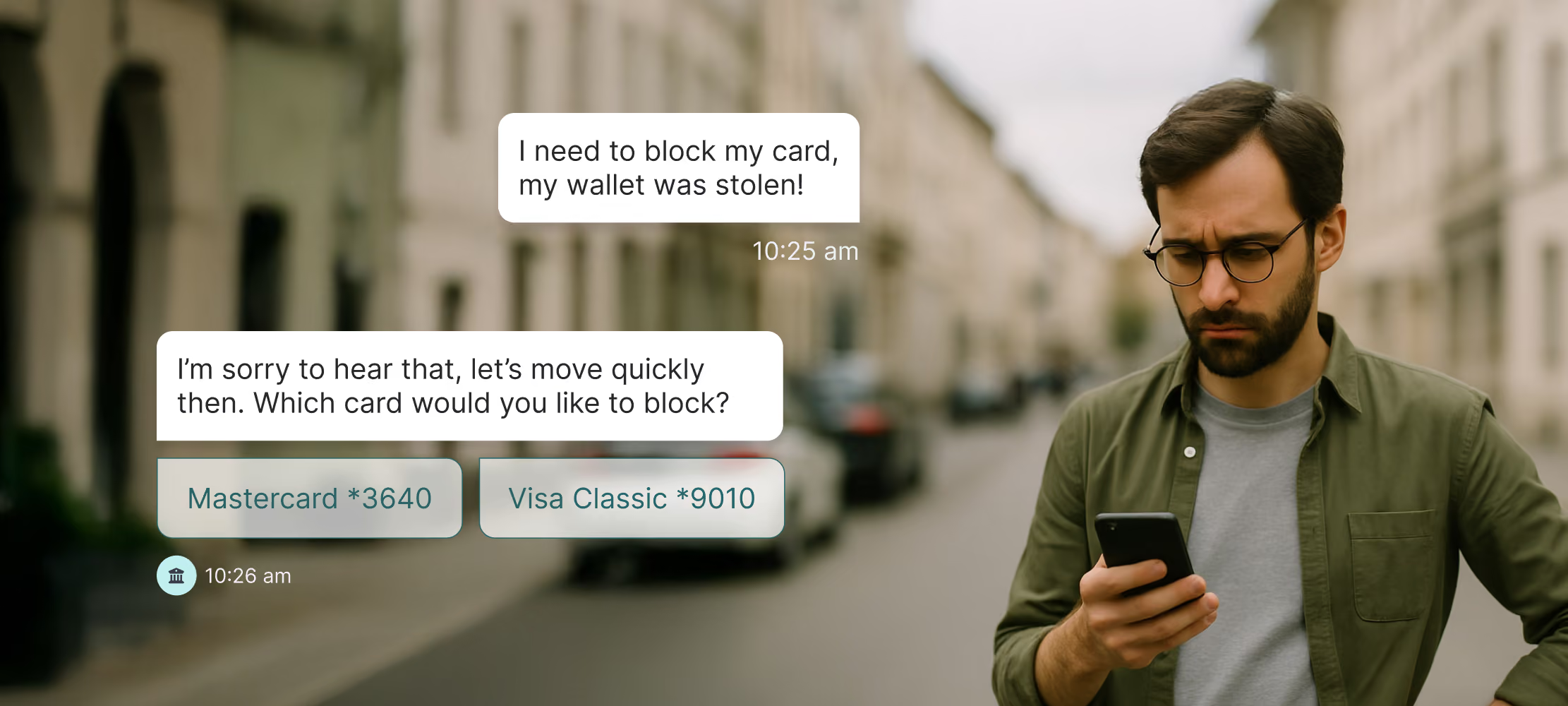

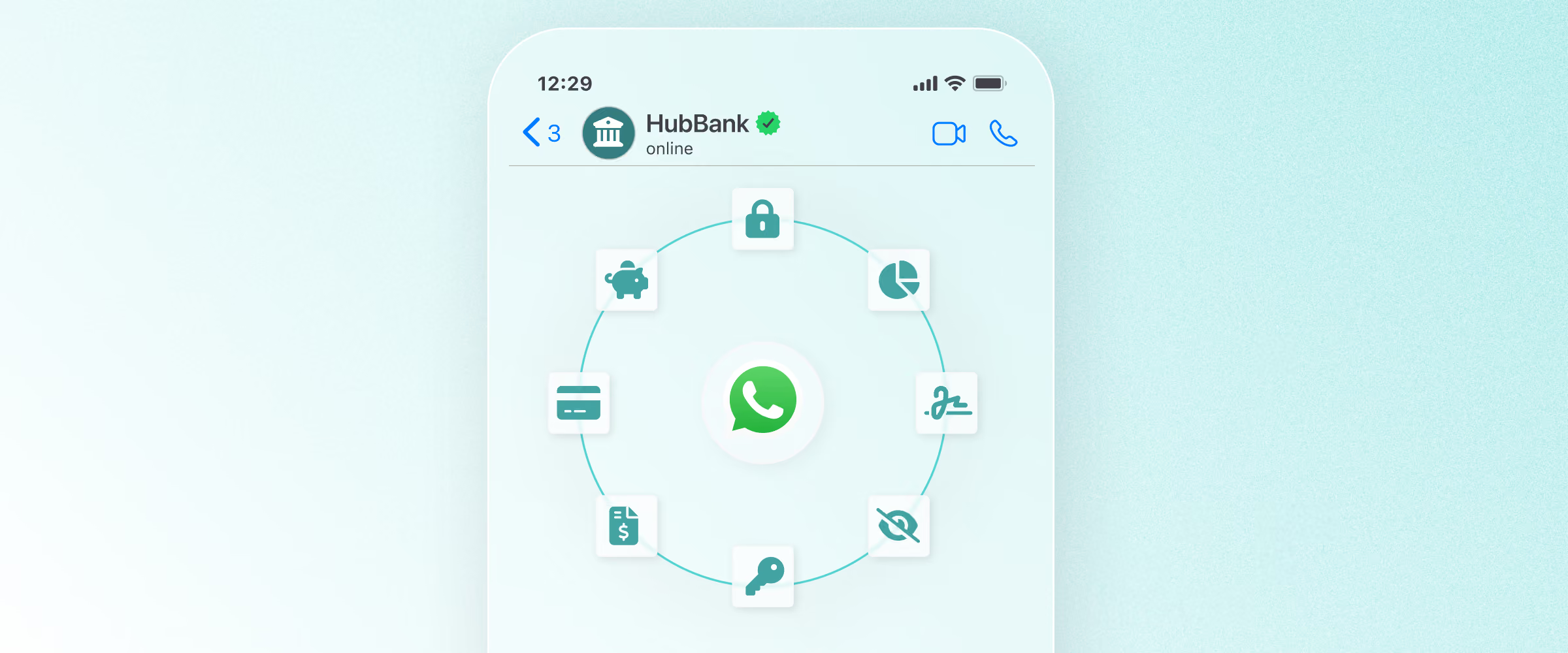

Conversational banking is a multi-channel approach to marketing, selling, and serving customers. It creates a cohesive customer experience no matter how or where a customer reaches out.

When given the option, most people want to reach out on messaging channels. WhatsApp, for example, is the world's most popular messaging channel. It has users in over 180 countries and sees 60 billion messages sent every day.

Moreover, conversational banking means meeting customers where they already are -- and they're on messaging apps. Using the apps they already use reduces friction in customer service in an impactful way. And, getting it right involves a purposeful use of automation.

Banks should bet on messaging

To be scalable, brands must use automation in their conversational strategies. But, the automation must actually be helpful and purposeful.

Unlike IVR, automation on messaging channels improves experiences -- instead of creating more friction.

Think about why IVR is so frustrating. Banks use it as a filtering system to route calls to the right customer service agents. Also, IVR alone rarely solves issues. Instead, customers face long hold times, long menus, and all-around poor experiences.

Automation, when combined with messaging apps, powers conversations that increase customer satisfaction. The combination allows businesses to provide always-on service and actually resolve most queries.

By combining messaging and automation, most businesses automate 80% of their queries. Sure, they enjoy cost savings as a result -- they handle more queries with fewer resources. But, that is not the main goal.

Again, substitution at a lower cost is not why challenger banks are winning. It's the streamlined experiences that they provide that makes them disruptive.

Meaningful automation on messaging channels is key to success

Meaningful automation actually handles predictable inquiries. It also hands-off questions to human agents when necessary. This frees up agents to do higher-value work and contribute to the team in more valuable ways.

Purposeful automation also powers unique experiences at scale. It uses customer details, product info, purchase history and more to personalize the customer journey.

Banks can keep customers engaged and make their experiences more enjoyable by incorporating interactive features, such as emoticons and GIFs. With buttons and rich elements, it's easier for companies to create a structured flow and guide customers towards a resolution.

The results are transformational for businesses. They enjoy increased customer retention, and increased lifetime value (LTV).

The bottom line is that the combination of messaging and automation is needed to be truly customer-centric. It's what powers conversational banking and what Fintechs use to deliver disruptive experiences.