How people manage their money is changing, and banks need to keep up. Consumers are looking for fast, efficient, and affordable solutions they can access anywhere. That’s why many financial institutions are cashing in on the idea of future-ready banking. But what really makes banking operations future-ready?

In this post, we’ll go over the main characteristics of future-ready banking operations, according to industry experts.

1. Distinctive, personalized products and services

The first characteristic of a future-ready bank is its ability to personalize products and services. Contextual personalization across the customer journey can only happen if banks have ditched legacy infrastructure in favor of modern solutions.

Modern infrastructure supports product and service development and delivery in ways that legacy systems cannot. It powers real-time, predictive, and proactive financial experiences that serve customers’ specific needs.

The need for personalized and consistent experiences has increased greatly over the past few years. According to @Jim Marous, financial industry strategist and co-publisher of The Financial Brand, “As branches became unavailable during the pandemic, the awareness of digital-native alternatives increased, with both consumers and small businesses ‘testing the waters’ with alternative providers that had created highly personalized digital solutions.”

“For bank and credit union marketers, increased confidence in digital banking products and services provided a surge in usage, and an opportunity for institutions to create improved levels of real-time communication and engagement,” writes Marous.

This means financial institutions must rethink their business models to provide hyper-personalized engagement at scale.

2. Speed, flexibility, and freedom

This idea of increased flexibility and freedom extends to more than just the type of services customers have access to, but also their overall user experience. For example the ability to sign documents online or through a mobile app.

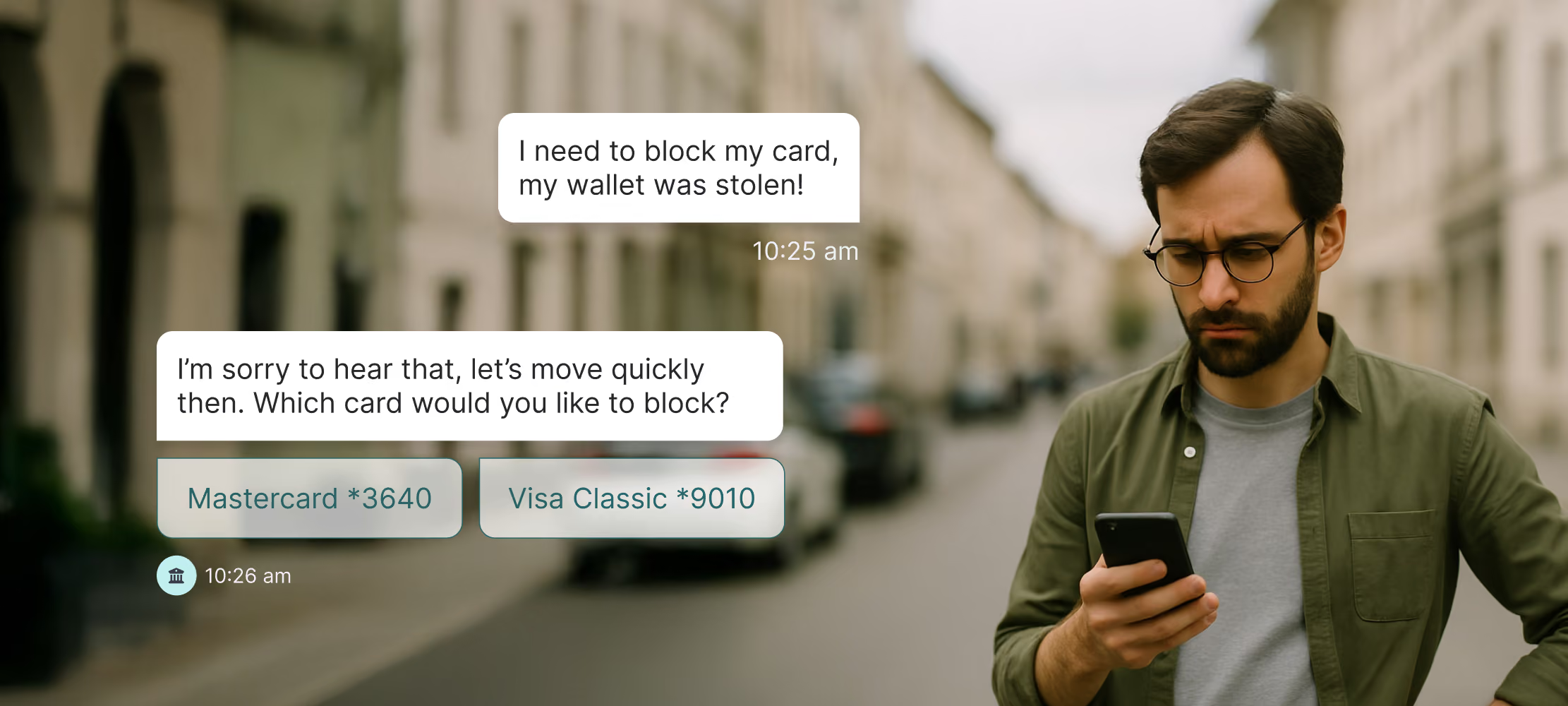

E-signatures alone have the potential to speed up the mortgage approvals process from a matter of weeks to minutes, as well as other operations such as call centers and customer service. However it’s really just about giving people the tools and options for better self-service.

@Chris Skinner, fintech advisor, and author at The Finanser, often speaks about the importance of self-service in banking, and the effect it can have on customer experience. “I spend so many times these days myself, sitting on a phone and getting a message that most of our operators are busy right now, please call back later or be prepared to wait until your life is no longer worth living that I give up. The majority of companies – banks, telcos, airlines, retailers and more – have moved into self-serve mode.”

By making the shift to digital self-service, banks can overcome this problem and allow their customers to get in touch anywhere, anytime and receive real-time responses to their queries.

3. Consistency

Everyday, operations staff carry out countless repetitive tasks such as reviewing debit or credit card disputes from customers or making sure payments are processed properly. However, studies show that as much as 48.8% of human error can be put down to repetition, so with these types of operational tasks, even the most highly-trained employees can make mistakes.

In fact, according to McKinsey, up to 5-10% of all debit card disputes in certain US banks are processed with errors. These errors can be easily avoided through the automation of these operations.

Not only does automation allow banks to provide an error-free and consistent service to customers, but it also frees up staff time which can instead be used to help customers with more complex or sensitive issues.

4. Proactive issue resolution

Future-ready banks have analytics in place to anticipate customer needs. They understand that great customer service is about being proactive—and doing so at a granular level.

“Reactive service experience places the burden on customers to find the best channel for resolution.” @Philip Jenkins, expert in advanced analytics and data management including predictive models.

That’s why, rather than waiting until a customer raises an issue, advanced analytics can identify any errors, such as a duplicate transaction for example, and alert the customer that the mistake has been detected and is already resolved. Being proactive in this way has a direct impact on customer satisfaction.

5. Less back offices and silos

The traditional banking structure has always been organized into three areas; front offices (branches), middle offices (call centers), and back offices (operations). However, with the way the industry is evolving, this structure will be impacted greatly, and it’s about time. The need for back offices and call centers will lessen, as banks begin to automate more customer service operations.

In order to eliminate back offices and silos, however, banks will need to think of their organization as an ecosystem—or an integrated network. The organization needs to have a fully-functioning “brain” or it runs the risk of getting stuck in a perpetual loop of silos.

Investing in the right technology, and working with automation specialists like Hubtype that understand these challenges can help. A recent report by McKinsey highlighted what can happen when banks invest in technology without a focus on creating a unified, centralized tech ecosystem.

In McKinsey’s example, a large retail bank invested in ML (machine learning) with the hope of improving its personalization initiatives, but after two years, it was still managing its personalization program the way it always had: manually and in silos. Although it had acquired a sophisticated analytics engine, the bank had overlooked the elements needed to turn that engine into a smoothly functioning “brain.”

This demonstrates how, despite investing in digital technologies, not all banks have been able to scale these successfully throughout their organization in a way which makes them truly future-ready.

Properly built tech ecosystems, however, will also empower organizational restructuring. Front office staff will be able to instead focus on the complex queries which can’t be done digitally, as well as give customers advice on bank products and features, like a personalized banking advisor.

6. Highly-empowered employees

Many other employee roles are also set to evolve exponentially in a future-ready banking environment. Employees will still need to have a deep knowledge of the bank’s systems and processes, but will need to hone the communication skills necessary to resolve complex customer issues.

On the future of banking, author, entrepreneur and expert in AI and fintech @Brett King notes: “Banking has to work when and where you need it. The best advice and the best service in financial services happens in real-time and is based on customer behavior, using principles of big data, mobility and gamification.”

That’s why certain roles which, up until recently, had little to no customer interaction, will now be critically involved in customer support. They may have tech, data, and UX backgrounds, and might include engineers, data scientists, and digital designers. All of which will be working to innovate and develop technologies for the improvement of their customer experience.

Is your bank future-ready?

The characteristics of future-ready banks are driven by modern technological solutions. Banks understand that they need to adapt, but are also afraid of investing in the wrong solutions.

At Hubtype, we give banks future-proof solutions to today’s problems. Our conversational technology helps banks personalize experiences, automate use cases, and unify channels. Book a demo with one of Hubtype’s conversational experts today to discover the future-ready banking solutions for your customers.