To be disrupted or to be the disruptor? That is the question for today's insurance companies. As new products, services, and business models emerge, the industry is about to reach a digital tipping point.

Insurance industry trends point to a harsh reality for insurers; adopt disruptive technology or die. The truth is, we're past the point of digitizing existing business models. Instead, businesses need to completely transform to survive.

Until recently, industry regulation provided a false sense of security

The industry, protected by regulation, has been slow to feel digital technology’s impact. Until recently, complex legislation has been a deterrent to new competitors.

Now, automation, advanced analytics, and blockchain are changing all of that. Technology has opened the door for real change, and investors are lining up to cash in.

In 2019, InsurTech investment reached an all-time high. $6.37 billion was invested in the InsureTech sector, and there was a 90% jump in investment rounds that exceeded $40 million.

These investments will drive innovation in an industry that historically has been slow to change. Leaders must take a proactive approach if they want to navigate these changes smoothly.

New, disruptive companies are proving that insurance doesn't have to be difficult

The insurance industry is still playing catchup when it comes to customer experiences. Customers expect a high degree of personalization and convenience. They also want innovative ways to shop for and manage their insurance policies.

For new InsureTechs, disruptive experiences come built-in. Let's take Lemonade, for example. Lemonade is a property and casualty insurance company that is, quite literally, changing the conversation in insurance.

Lemonade's insurance chatbot Maya, can onboard customers in as little as 90 seconds. And, let's not forget about Jim, a claims chatbot that can settle claims within seconds.

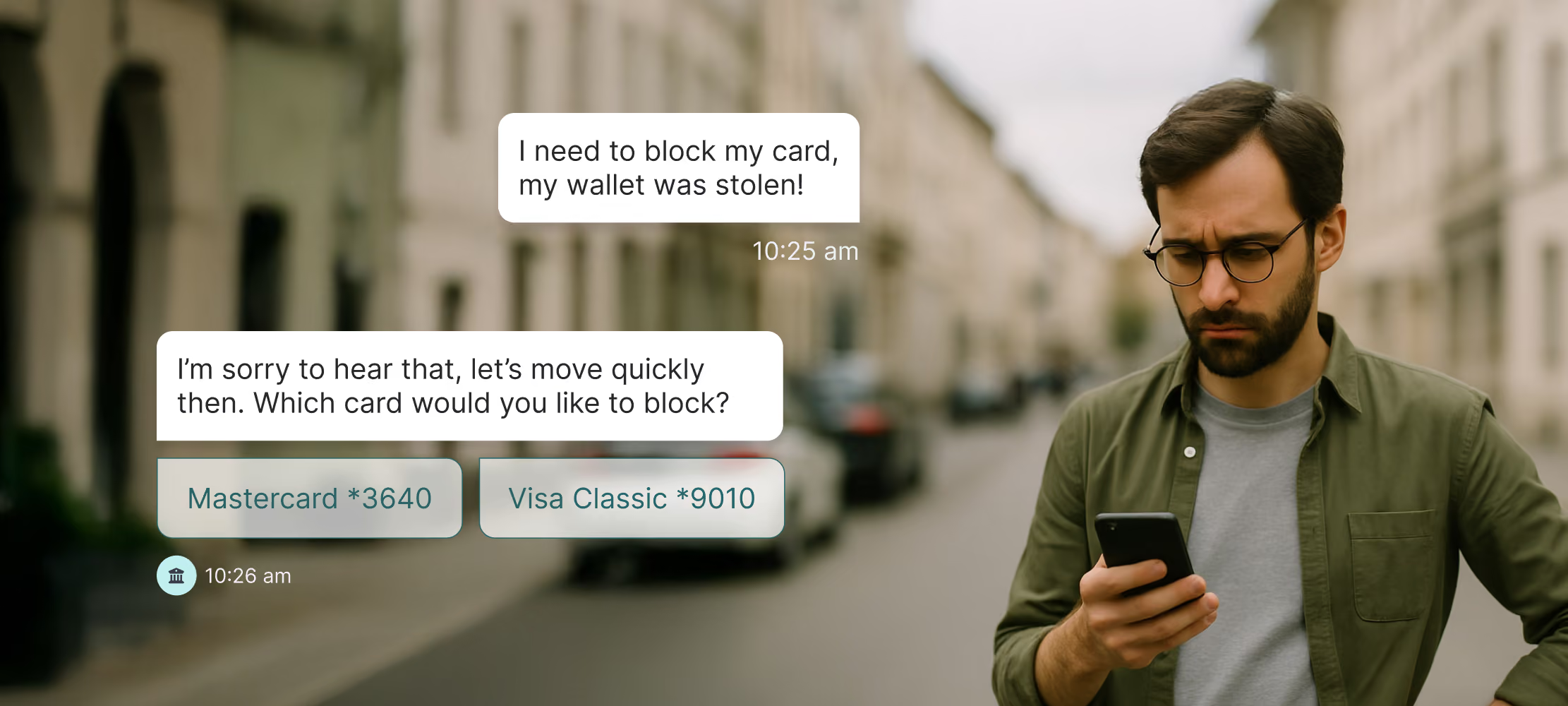

Conversational apps have emerged as a solution to simplify frustrating processes. The process of submitting a claim, for example, is where most customer pain-points are realized.

No one wants to have to submit an insurance claim, and doing so is usually the result of a car accident, property damage, or other stressful situation. Customers often become irritated by a lack of visibility into when they will be helped to recoup their loss.

Conversational apps and automation are addressing those pain points. With meaningful automation, customers don't have to repeatedly answer the same questions. They experience less friction and are generally more satisfied. This is a big deal for industry leaders seeking to improve LTV (customer lifetime value). What's more, automation reduces the cost of a claims journey by as much as 30%. It drives long-term operational cost reductions and savings that can be passed on to the consumer.

Legacy systems aren't the bottleneck they once were

Legacy systems have long been a barrier to innovation. The insurance industry relies heavily on IT systems, many of which need to be modernized.

Thankfully, those legacy systems aren't the obstacle they once were. Today, APIs (application programming interfaces) make it possible for businesses to adopt new technology without ripping out their old systems.

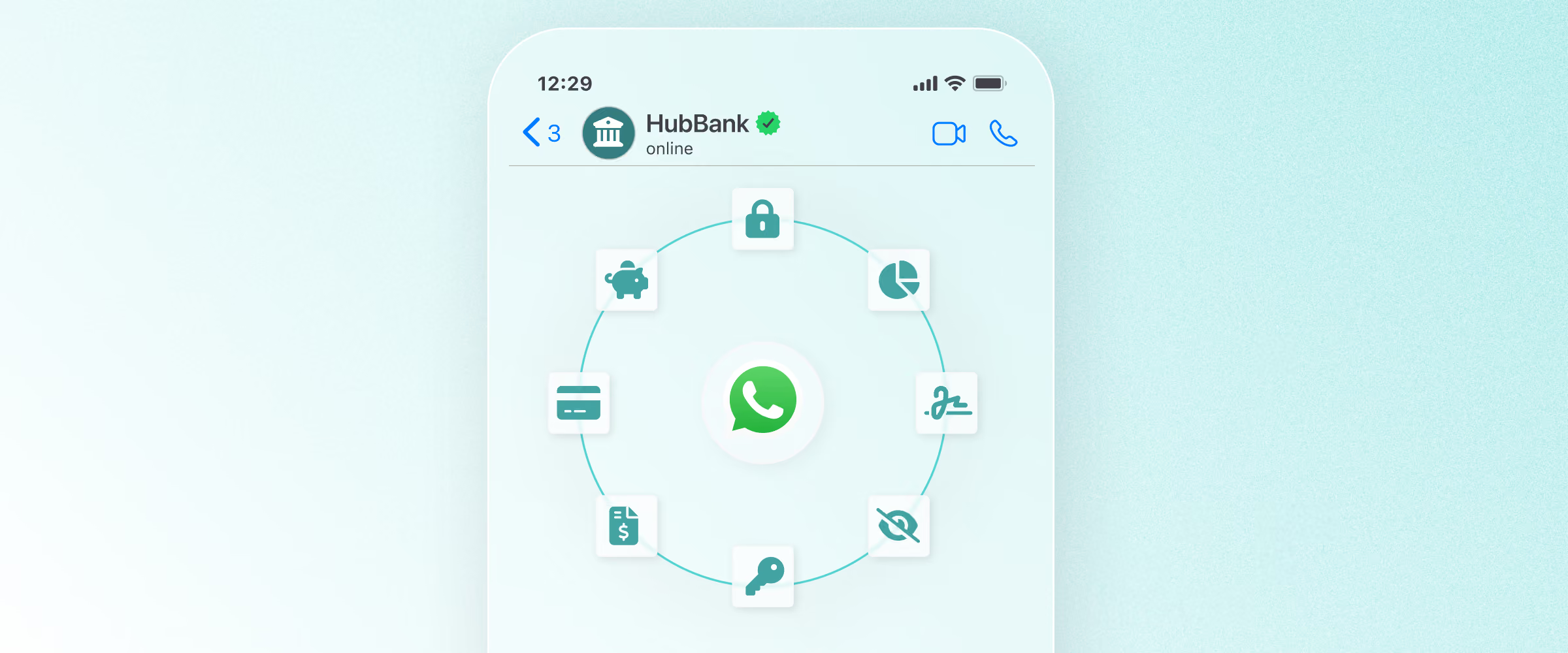

For example, at Hubtype, we help all types of enterprise businesses with their conversational strategies. Because we can integrate with anything, even companies with older systems are able to use conversational apps to serve customers on messaging. The world’s leading banks and insurers trust Hubtype to safeguard their customer communications.

In short, APIs even the playing field. They make it possible for traditional insurers to compete with new market entrants who are starting from scratch with modern and simplified systems.

Technology finally addresses data privacy concerns

Until recently, using data to personalize products for different customers was yet another challenge. The complex regulatory landscape, along with data protection laws, have been a major hurdle.

Now, through end-to-end encryption and flexible technology, insurers finally have options. With a focus on security and compliance, platforms like WhatsApp make it possible to create conversational experiences that are both excellent and secure.

Conversational apps are the way forward

It's clear that change is inevitable for the insurance industry. Insurers must find ways to keep up with the people that they're insuring.

As shown in the Lemonade example, conversational apps and interfaces address the challenges at hand. Through conversations, brands can simplify experiences and make insurance less complicated.