The revised Payment Services Directive (PSD2) isn't 'just another regulation.' It will accelerate the already on-going digital transformation in banking.

The goal of PSD2 is to make the European financial industry more competitive -- and it will. The regulation forces banks to share customer account information with qualified third-parties.

As a result, new market entrants can now compete with traditional banks, in ways that were previously impossible. European banks face unprecedented competition from Finacial technology (fintech) companies, smaller banks, and new players. To remain competitive, banks must act now.

It won't be enough for banks to approach PSD2 as a practice in compliance. Doing so opens the door for third parties to come in and meet their customers’ changing needs.

Instead, PSD2 must be approached as an opportunity for a digital transformation in banking.

How banks can remain competitive

Compliance with the new legislation means that financial institutions must provide information about their customers’ bank accounts to third parties via APIs (Application Programming Interfaces).

APIs are fundamental to the digital transformation in banking. Today’s banking infrastructure relies on established legacy systems, which are one of the greatest obstacles to innovation.

APIs solve this issue by allowing banks to build on top of legacy systems and mainframes. As a result, they gain agility and freedom to innovate.

Although APIs unlock a world of opportunity, many banks have been slow to adopt them. Now, it's no longer an option. European banks are required to develop them before December 31, 2020.

So, the time is now for banks to use those APIs to solve consumer pain points that are still not being addressed. If they don't, someone else will.

The easiest way to stay competitive is to partner with third parties rather than view them as the enemy. APIs set the stage for better collaboration and adoption of customer-centric, digital solutions.

The bank of the future

It makes little sense for banks to build new solutions on their own when partnerships can provide instant technology and market access to service clients. So, collaboration is a clear way forward.

Banks should use their APIs to add new services and technology without adding huge costs. They can focus on their core competencies and rely on third parties to digitize the customer journey.

In this way, banks will be able to rapidly improve their business models. One part of the banking business model ripe for change is customer service.

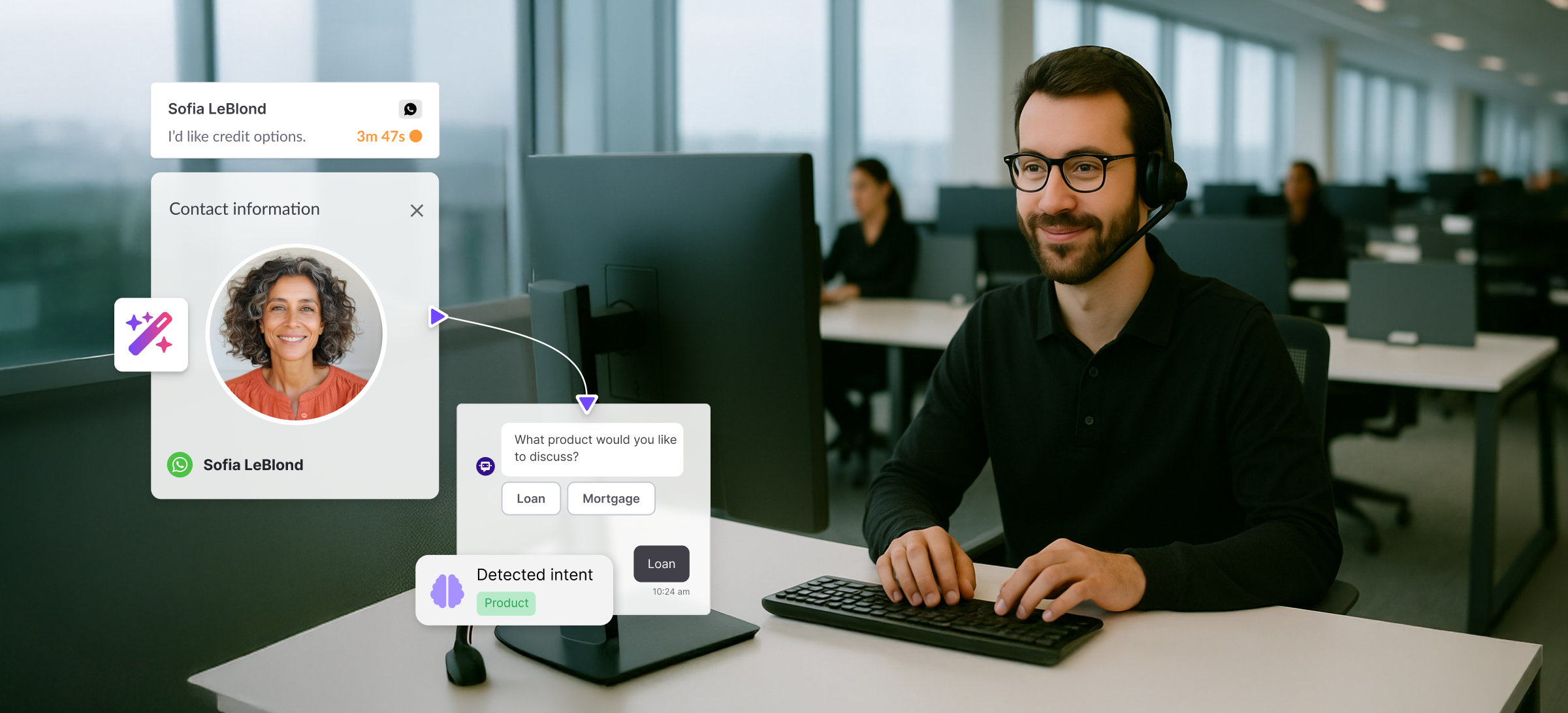

Part of what makes fintechs so disruptive is their ability to reinvent customer service. Following suit, banks should choose to partner with companies that prioritize

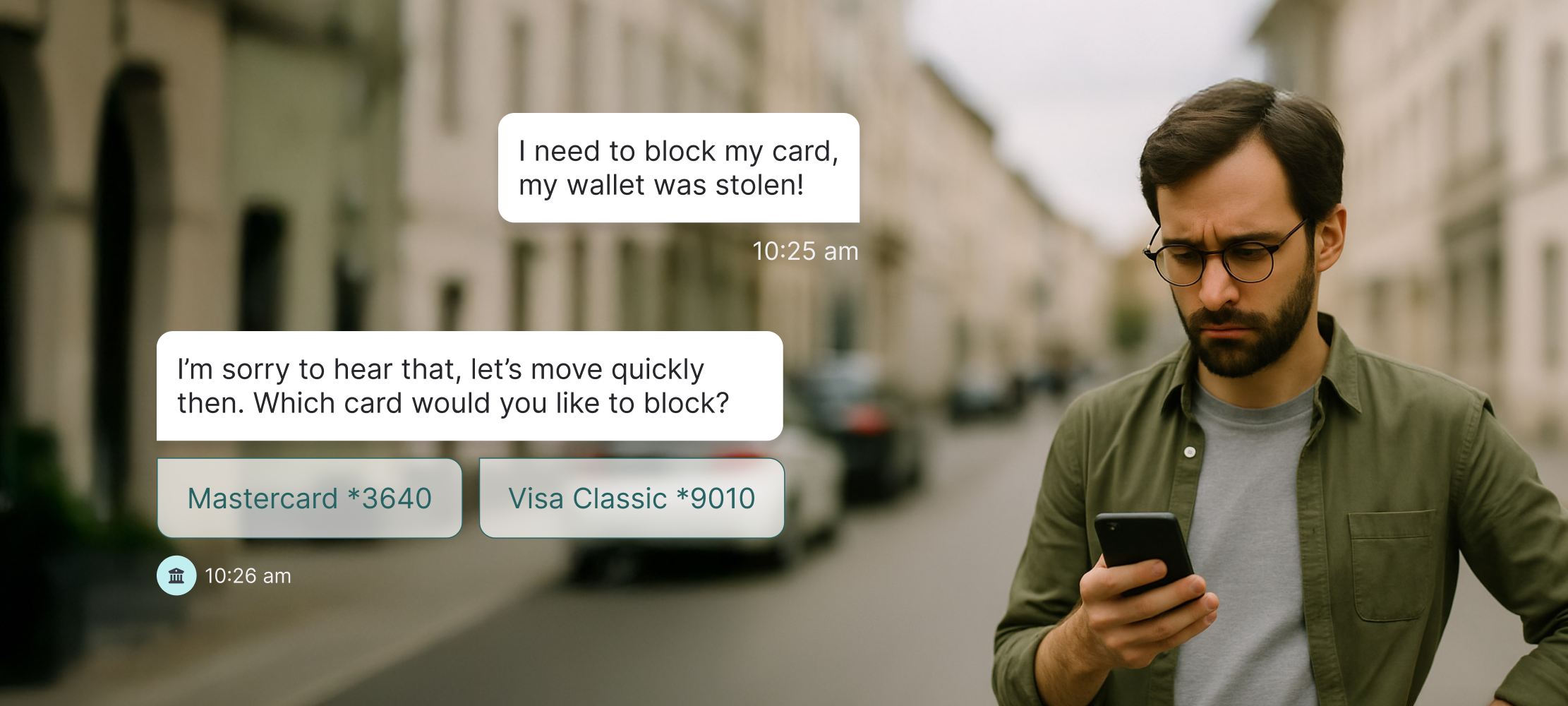

- 24/7 access through purposeful automation

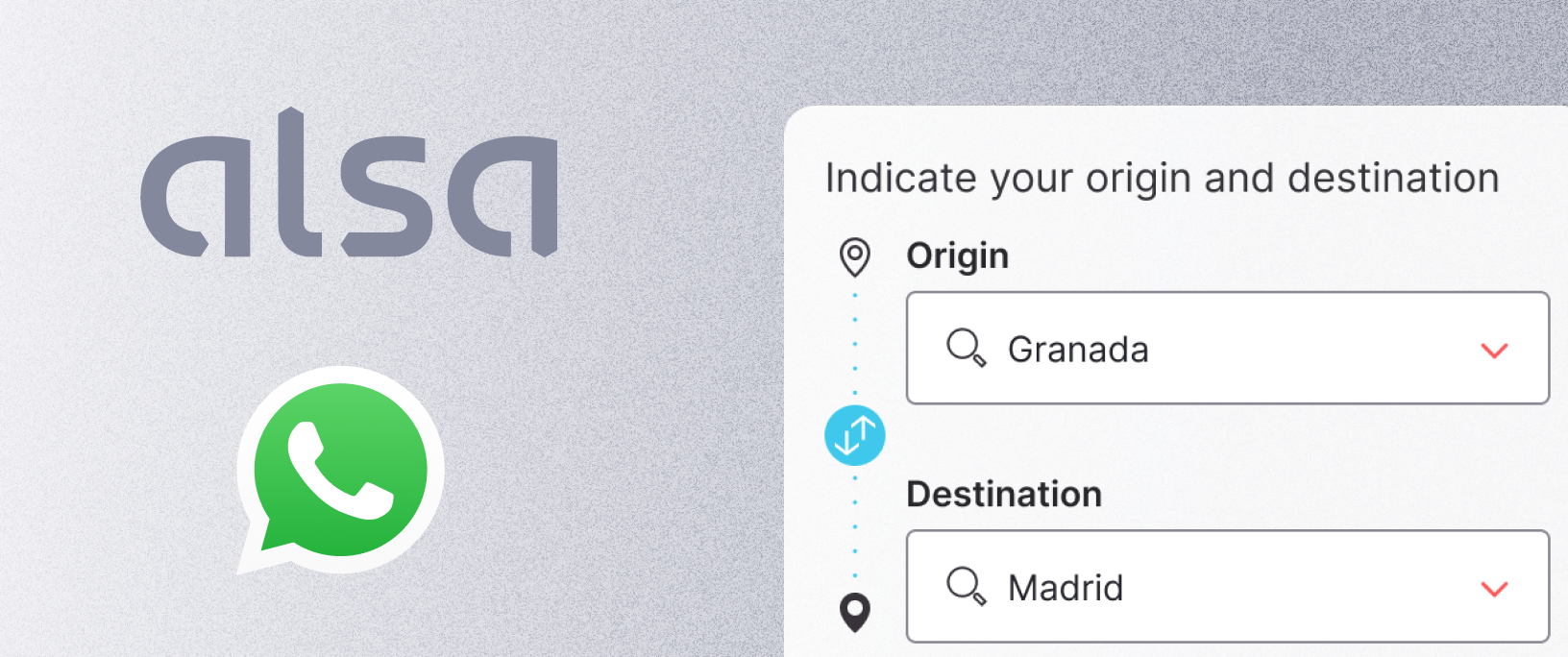

- service via non-traditional channels like WhatsApp and social media

- seamless customer service across all channels

How Hubtype helps

At Hubtype, we partner with the world's leading banks to help them transform their customer service models. We help banks like Caixa Bank and Bankia deliver intuitive digital experiences through conversational apps.

Our conversational platform allows banks to adopt an omnichannel customer service strategy -- without building backend infrastructure and interfaces.

Hubtype integrates with WhatsApp, Facebook Messenger, Web Chat, Viber, Line, and other messaging channels, so banks can meet their customers how they prefer.

Especially in the wake of COVID-19, banks rely on us to increase their operational efficiency. We take a human approach to automation, helping banks purposefully automate components of the customer journey while empowering their human agents.

We also know how important it is for banks to comply with privacy and security legislation. Our tools and workflows are designed to protect banks and their customers at all times. Through rigorous penetration testing, we provide our financial clients with enterprise-level security and GDPR compliance. Learn more about how Hubtype moves banks forward here.