We have a lot to learn from the rise of challenger banks. Challenger banks are winning a war for customer engagement -- and the industry is taking notice. In 2019, the global fintech sector had another blockbuster year, reaching $135.7 billion invested across 2,693 deals.

Yet, despite this rapid growth, traditional banks still have an upper hand. They still have the lion's share of the market, large customer bases, and powerful brand visibility. But that doesn't mean that they can rest on their laurels.

Though neobanks (app-only banks) and fintechs have made relatively small inroads, the implications are significant. Fintechs are changing what banking means to people. They're driving a rapid evolution in customer expectations.

So, how quickly do traditional banks need to move to meet these new customer expectations? Sooner than you might think. Regulatory changes are removing barriers to entry, making it necessary to adapt now.

Banks who can combine the power of their legacy with the disruptive mindset of challenger banks have everything to gain.

What we can learn from the rise of challenger banks

1. Seamless customer experiences are the shortcut to success

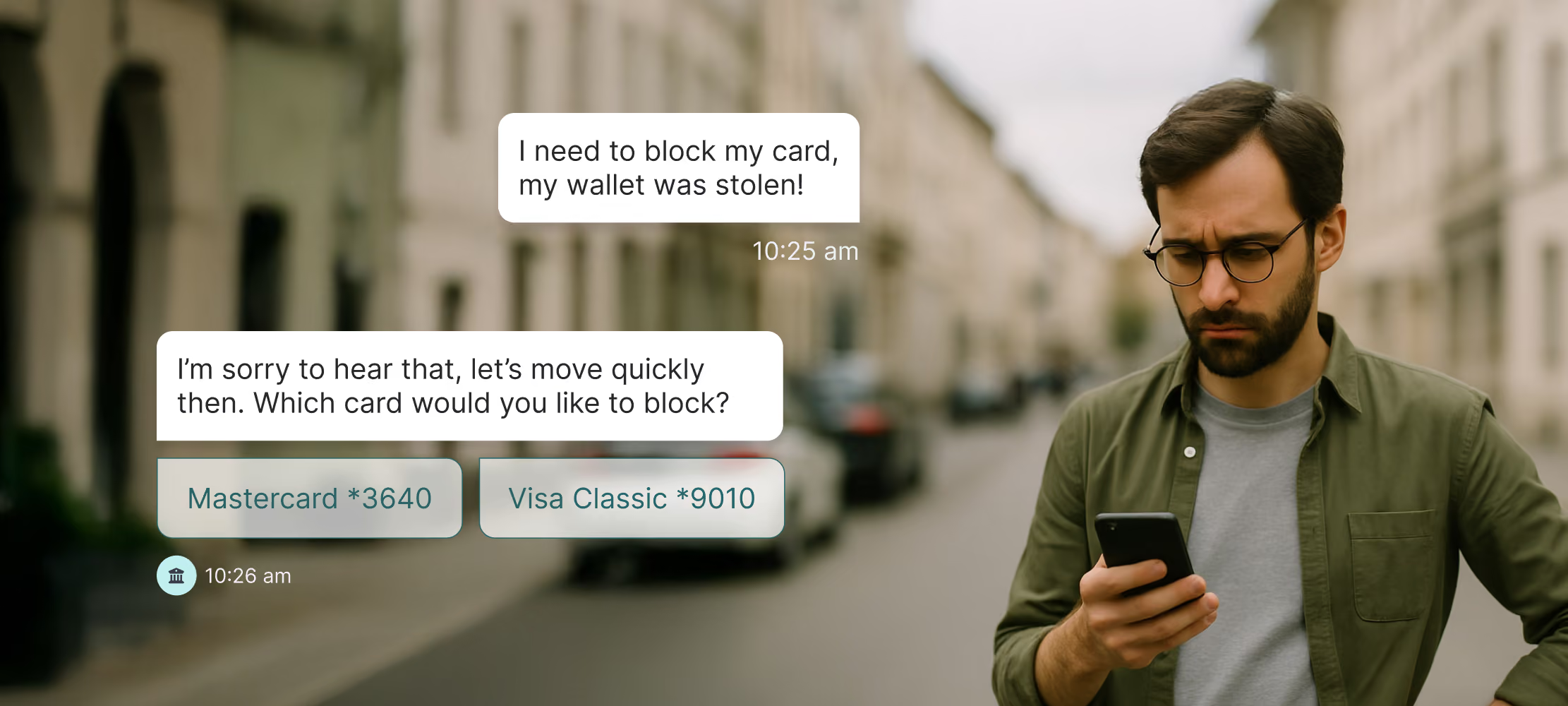

Traditional banks must reimagine and reshape their customer experiences. And, they need to start with what their customers actually want. Spoiler alert: they don't want more automated voice recordings and long hold times.

Customers want and expect simple, seamless services. They expect quick answers to simple questions. They don't want to have to go to physical branches. In short, they want streamlined transactions at all touchpoints.

How do successful fintechs and neobanks create seamless customer experiences? Through conversational banking.

Conversational banking is a multi-channel approach to marketing, selling, and serving customers. It creates a cohesive customer experience no matter how or where a customer reaches out.

There are many aspects of conversational banking that excite digital innovation leaders. One of them is the use of purposeful automation. Until now, it's been difficult to create automated experiences that make things go more smoothly. With conversational banking, customer satisfaction scores actually increase alongside operational efficiency.

2. Digital natives will fuel future growth

Fintechs an neobanks successfully cater to digital natives. Digital natives are those of us who were brought up during the age of digital technology and so familiar with computers and the Internet from an early age.

According to Citrix, almost 50 percent of workers today consider themselves to be digital natives, and that number will increase to 75 percent by 2025.

To resonate with that audience, fintechs are building experiences that are very similar and comparable to Spotify, Uber, and any other great apps.

Valentin Stalf, CEO of neobank N26, explains:

"We tried to actually build something without looking at traditional banks, but built something from scratch as you would build it for a digital native. I think we have done a pretty good job. Our customers like the product; you can, for example, sign up within five minutes, you don’t have to sign any papers, you get your card a couple of days later and I think we just tried to have a really cool digital native experience."

3. Personalization is key

In many ways, challenger banks take notes from online retailers like Amazon. They show their customers relevant products and services, or even offer them ones they had never thought of.

For experiences to be exceptional, they need to be relevant and personalized. Solutions should align with a person's life events and unique needs, with businesses anticipating their needs at every point in their customer journey.

The issue of scale makes these types of contextual experiences a challenge; that's why technology is fundamental to creating them. To provide fast, personalized service to customers at scale, purposeful automation is necessary.

4. A transactional mindset is not enough

Financial planning tends to come hand in hand with major life changes. For example, buying a new home, applying for a new business loan, or starting a college savings plan for a child. And, banks have the opportunity to be a consumer’s first choice in navigating these needs.

Instead of looking at banks through a transactional lens, they have the chance to be interactional. They can listen to the goals and life plans of their customers and help realize them through financial services.

Banks that are able to really listen and engage in a two-way dialogue will form deeper customer relationships. And, those relationships foster higher lifetime value and loyalty.

5. Conversational apps are the way forward

Unsurprisingly, technology is the key to helping traditional banks compete over the next few years. Conversational apps are a driving force behind the rise of challenger banks.

The growth of messaging, the democratization of automation, and the rise of mobile have created the perfect environment for conversational strategies to flourish. Over the next few years, it is not a matter of if banks and insurers will adopt conversational strategies — but when.

Not sure where to start? At Hubtype, our experts make it easy to understand which conversational banking options are right for you. Our technology is scalable, flexible, and ready to grow with you and your customers.